Capital Allocation into European venture capital: potential met by structural fragmentation (SOET25)

The following borrows heavily from the State of European Tech 25 (SOET25) report which I strongly recommend for anyone keen about the future of the venture capital and startup ecosystem in Europe. A read through is well worth your time.

A common theme that emerges is that Europe has the ambition, talent and capability to scale its tech scene but it is bogged down by structural fragmentation. This occurs, in my opinion at two levels: the startup development and growth level and at the capital allocation level.

At the startup level, Europe can point to stories like Revolut, Lovable and n8n and show how with the right mix of talent and capital, success can be built in Europe, yet many scaleups still look across the Atlantic when it’s time to scale. A fragmented European market means that the US outcompetes Europe not only because of deeper capital pools, but also because scaling in Europe means addressing 27 distinct markets, each fragmented and presenting cultural, legal and regulatory obstacles.

The European Commission has promised to create a “28th regime” allowing startups to scale across the continent, with more than 15,000 people already having signed EU–INC’s petition to get the Commission moving on its promise, for a single, simple, framework that lets startups compete without legal friction.

Capital Allocation in European Venture

This essay focuses on the capital allocation side of the European market as presented in the SOET25 report. Here again we shall see that potential for capital to be invested into high growth potential talent and innovation is already present but remains sorely undertapped. Once again, it is structural fragmentation that is holding the continent back.

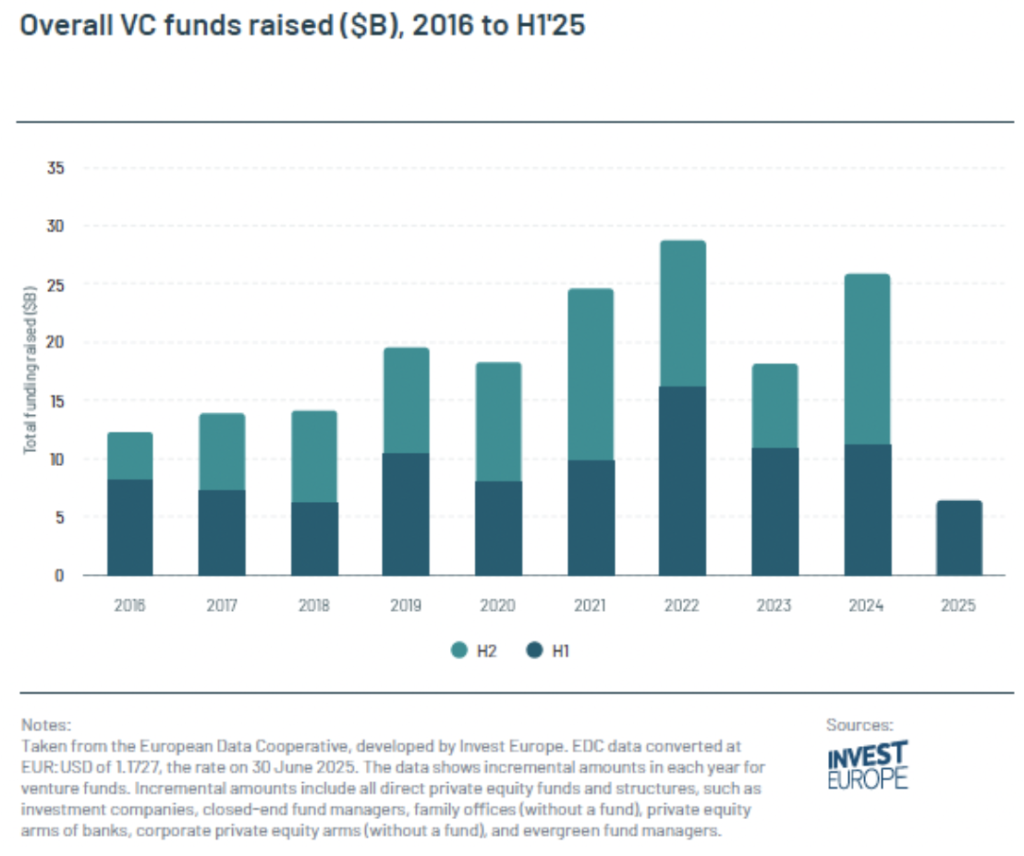

In the second half of 2024, VC funds raised more money than in almost any other half-year period over the past decade at just under $15B, putting it on par with H2 2021. This year paints a far more mixed picture. While fundraising data suffers from a degree of reporting lag, current estimates for H1’25 indicate a significant softening, with fundraising back down to $6.4B. Yet, signs of an improved market condition are apparent: Prague-based Aspire11’s inaugural €500M fund draws from pension capital (The Partners Group is identified as the major limited partner (LP) and pension-capital contributor). The strategy is to connect long-term pension capital with venture capital.

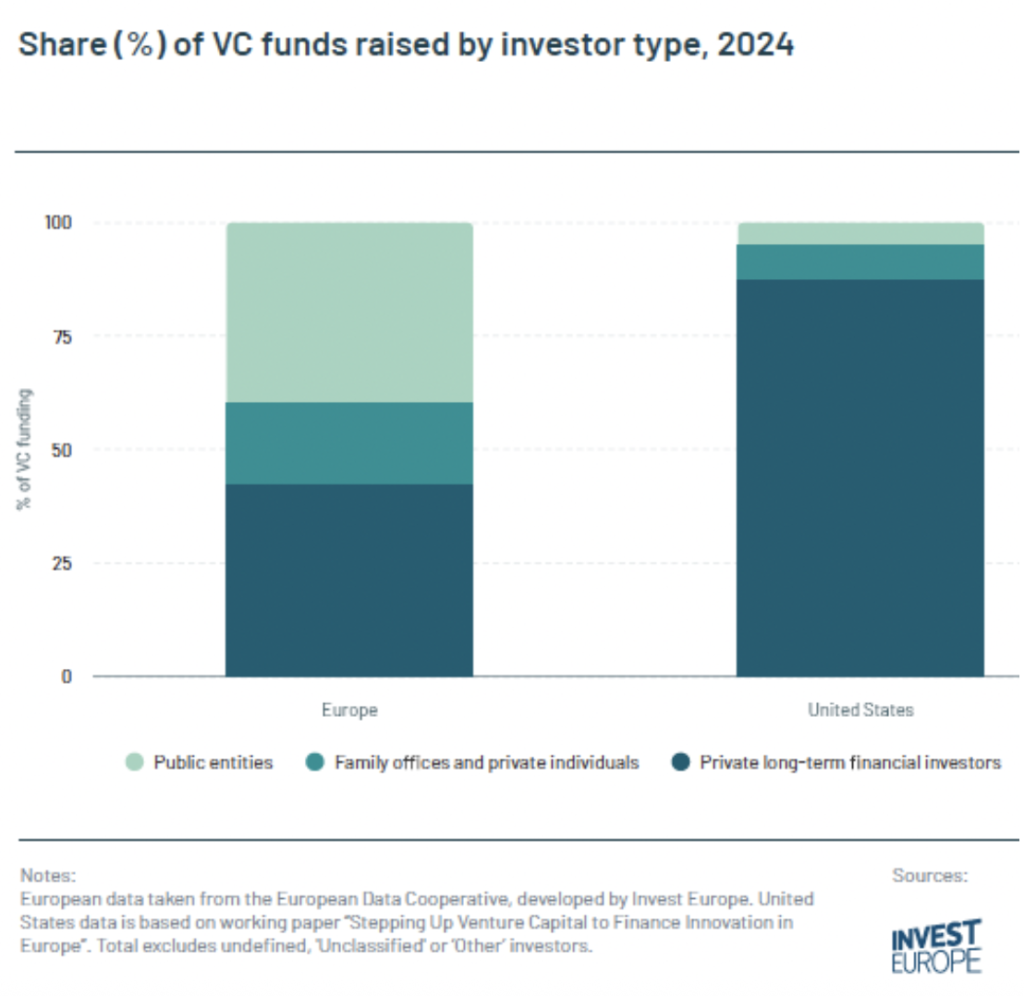

Private long-term investors make up almost 90% of the investors backing US VC, compared to 42% in Europe. Europe has no equivalent of Yale’s $40B endowment to tap for funds. Instead, it relies more heavily on public entities, which make up 40% of the long-term investor pool compared to 5% in the US. Family offices make up the remaining 18% of the long-term investor base in Europe.

While 2021 and 2022 introduced some private players to the European VC scene, those investors seem to have retreated, following a general international industry trend, leaving government funding once again as the ecosystem anchor. The largest contributor in this category by far is the EIF, which supports the ecosystem through initiatives like European Tech Champions, a fund-of-funds launched in 2023 to provide late-stage capital to European startups, alongside direct investments in VC funds. Last year, every $1 of government funding put into venture capital was matched by $2.9 elsewhere, almost in line with the long-term average of $3.3 between 2016 and 2024. During the peak funding years, the multiplier effect was the highest when every $1 invested by governments was matched with another $4.9 from other investors.

In 2024, the EIF made over 100 investments into VC funds across all European regions, representing a 30% increase in transactions. In 2023, the EIF’s largest commitments included a $380M injection to Headline Global Growth Lux IV and $300M into Atomico’s Growth VI fund.

While US pension funds and endowments have embraced venture, most of Europe’s institutional capital remains tied up in more conservative allocations, favouring fixed income strategies and public equities over high-growth alternatives like VC. According to SOET25, the consequences are two-fold: these investors miss out on the upside of European tech, and the ecosystem itself misses out too, weakened by a lack of long-term domestic capital that causes success stories from home to leak. PlanRadar, an Austrian startup currently valued at $400M, illustrates this conundrum. European pension funds based in Germany and Austria own just 0.2% of the company today, while 8% is owned by US pension funds. When it exits, it is US investors, not Europeans, that will pocket the rewards of European innovation.

With the right allocation shift, European pensions and sovereign wealth funds could capture far more of the upside generated by the next generation of European champions, while also growing their own funds. What is needed is alignment of incentives for fund managers to shift focus towards risk-adjusted returns moving away from a culture of wealth protection to a much needed capital allocation strategy that considers growth at a European level as a key metric. The Norwegian’s sovereign investment fund decision to not allocate to private unlisted companies left a potential $80 billion (5% of its AUM) hole in the coffers of [mostly] European tech.

[Side note, the NBIM research on private equity is a great read]

Unlocking pension funds

The share of European pension fund AUM allocated to European VC in 2024 is 0.01%. Between 2023 and 2024, the absolute amount rose by 55% from $650M to $1B. Pension funds in particular remain underweight on venture capital compared to their peers in the US, who typically allocate around 0.03% of AUM to venture capital. Underinvestment leaves the door open for foreign investors to step in and capture the upside of Europe’s innovation, or for companies to leave Europe to achieve their full potential abroad. US pension funds invest 3x more into VC than their European peers. European pension funds only invested 0.009% of their total AUM into VC in 2024, while US pension funds invested 0.028%.

The additional capital that could be made available to Europe’s venture ecosystem over the next decade if European pension funds matched investment levels of leading US pension funds is a staggering $210B according to the SOET25 report.

European pension funds, sovereign wealth funds, and other long-term investors often cite predictable DPI as a key hurdle to allocating more capital to venture.

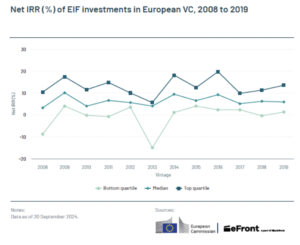

Over a 10-year horizon, the European VC index returned 17.2% compared to 13.1% for US VC and 13.7% for US public equities. The gap narrows over a 15-year horizon, but European VC still leads with a return of 16.7%. The EIF’s track record proves that exposure to a broad portfolio of European VC funds, which in turn provide exposure to thousands of companies, is a powerful diversification strategy and not as risky as often assumed.

While European VC portfolios outperform the market on unrealised valuation, European funds underperform compared to the US on Distributed to Paid-In Capital (DPI). In other words, LPs aren’t seeing their gains turn into real cash at the same cadence. Most European vintages have not provided meaningful distributions over the past two years. While 2023 was a strong year for returns, DPI gains were uneven across vintages. This creates a ceiling. LPs who are investing in the US and enjoying more predictable distributions are less incentivised to increase allocations to Europe until liquidity improves. No matter how much fund sizes or company valuations grow, this will continue to limit the European ecosystem unless it’s solved.

Structural limitations in Europe’s exit pathway

Over the past decade, $1B+ exits accounted for 86% of the value created by IPOs and 68% of value from M&A, despite only representing 13% and 0.7% of total deal count, respectively. In the US, there are three times as many buyers capable of leading deals valued at $500M or more, while Europe’s pool of buyers is almost exclusively concentrated in transactions valued under $250M. Europe may only be home to less than 10% of the world’s IPOs, yet this year it has produced two of the world’s 10 most valuable public debuts. September saw Klarna’s $17B IPO, the world’s fourth-most valuable so far this year, while SMG’s debut ranks 10th at $6B.

European listed tech companies are worth about $1.7T combined, just 5% of the US’s $37T. The 20 highest valued European tech companies (the Tech Titans) have been trading roughly on par to the NASDAQ-100 tech index, showcasing that Europe already has all the right ingredients to build global leaders. Unlike the US, whose market is concentrated on two dominant stock exchanges, in Europe value is spread thinly across 36 different exchanges, diluting visibility and liquidity even further. Europe’s entire tech market could fit into the NYSE three times over. In the US, the Nasdaq and NYSE account for 99% of tech company public market value, meaning there are obvious destinations for investors and tech companies looking to trade equity. In Europe, no single exchange has reached that kind of critical mass. Value is scattered across the continent, making it harder to convince European firms that this is where they can continue building value. Because of its relative size, the US can rely not only on companies built within its borders, but also companies from abroad who are attracted by the depth of liquidity to continue boosting its market cap.

Europe’s private markets remain too shallow to provide the scale-up capital needed to turn promising startups into global leaders. Late-stage rounds are smaller, scarcer, and slower than in other major ecosystems. And when companies reach maturity, they encounter fragmented public markets that lack the depth, liquidity, and sophistication to support European champions with truly global ambitions.

Some solutions are being proposed:

Savings into Growth – Empower Europeans to put their savings to work — productively, responsibly, and confidently. Unlock Europe’s €10T in household savings by advancing the Savings & Investment Union and treating financial literacy as core infrastructure, so citizens can share in Europe’s growth and future prosperity.

One Listing, One Capital Market – Build a single, liquid European market for growth companies by harmonising disclosure, pooling liquidity, and strengthening analyst coverage, creating a true “European NASDAQ” to keep IPOs, ownership, and value in Europe.

In my last 6 years at a US based venture capital firm it has become apparent that whilst media and social media commentary is focussed on the glamour of startup investments, with rock star founders and $billion dollar valuations, the capital allocation aspect, which is the fuel that funds the industry is a mostly underrepresented facet. In Europe, the European Investment Fund (EIF) is central to activity, while the US presents a more nuanced reality with private players such as pension funds, endowments being key players alongside HNWI and family offices.

Following this article I intend to dive deeper into this topic with coverage about the key private players in the capital allocation market in Europe as well as an understanding of the business economics of a fund-of-funds allocator amongst other potential topics.

Stay tuned, and wishing all readers a prosperous new year ahead.

Author bio: Adrian is a venture capital and portfolio management professional for early-stage startup investors.

For more information: www.clutchplayadvisors.co

Leave a Reply